A Standard and Clean Series A Term Sheet

Yaaaay! A standard, clean, just the facts. “Series A” term sheet by Y Combinator.

Nice! I am definitely keeping that!

A Standard and Clean Series A Term Sheet

While working with companies in YC’s Series A program, we’ve noticed a common problem: founders don’t know what “good” looks like in a term sheet. This makes sense, because it is often, literally, the first time in their careers that they’ve seen one. This puts founders at a significant disadvantage because VCs see term sheets all the time and know what to expect. Because we’ve invested in so many founders over the years and have seen hundreds of Series A term sheets, we know what “good” looks like. We work with our founders to understand where terms diverge from “good”, what they can do about that divergence, and when and how it makes sense to negotiate.

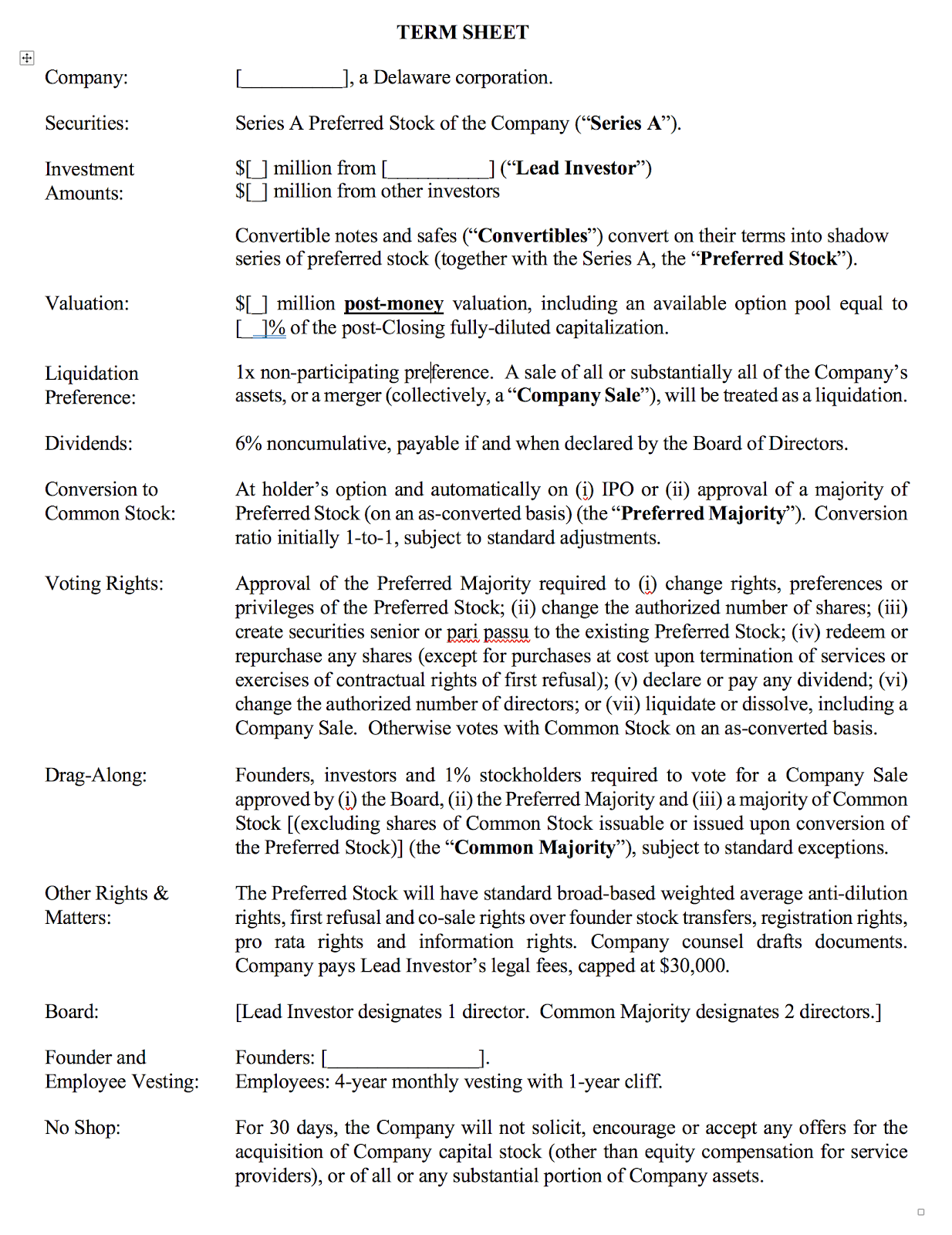

Below is what a Series A term sheet looks like with standard and clean terms from a good Silicon Valley VC. Bracketed items (besides the names of the company and lead investor) are always or frequently negotiated. Items not in brackets are sometimes negotiated, but this has more to do with the idiosyncratic features of the company or the situation, and generally aren’t terms that parties intend to heavily bargain over during the negotiation.

One of the critical things you’ll notice is that we didn’t put in standard pricing. While the lead in a Series A round generally wants 20% of the company, pricing can flex up and down depending on the leverage held by each side. We think price is an important term, but too specific to each raise to try to create a standard. We’re more concerned with terms around control and structure that are less familiar to founders, and therefore more prone to cause confusion and trouble.

Note: this term sheet doesn’t belong to any particular VC — we drafted it — but it does substantively reflect what we see most often. Founders with a lot of negotiating leverage can sometimes do better, and the converse is true too.

You can also download the Google version of the doc here .

It may be surprising to see everything covered in a single page.1 This wasn’t always the case, but became common over the last decade as some investors decided to make their term sheets more user friendly by shortening the legalese as if to say, “We aren’t going to get bogged down in the minutiae. We’re going to make this easy, friendly, standard and fast.”

This leads us to the most important thing to understand about the term sheet: it’s another way in which your Series A investor might be telling you something. A contract allocates risks between the parties, so the terms the investor insists on can sometimes say a lot about the investor’s perceived risks. These perceived risks show up in a couple of ways.

The first way relates to control terms. We don’t mean the set of investor vetoes in the “Voting Rights” section, which are pretty standard fare,2 but rather issues of board composition and the investor’s ability to block or dictate operational decisions made by the board. The board structure in this term sheet is founder-friendly because the founders retain board control 2-1.3 The way in which founders most often lose control at the Series A is with a 2-2-1 board structure, i.e. 2 founders, 2 investors and an independent board member. The loss of board control is most significant because it means the founders can be fired from their own company.4Another way in which founders lose some control is a term that doesn’t appear in the standard example above, which is a separate provision that says the investor director’s approval is required for operational decisions like setting the annual budget, hiring/firing executives, pivoting the business, adding new lines of business, etc. When boards are set up to take power away from founders, the investor’s outward justification will frequently be reasons of governance or accountability. But the more power that’s taken away, the more it’s undeniable that the investor is attempting to structure away a perceived risk. So when an investor says that they’re committed to partnering with you for the long-term – or that they’re betting everything on you – but then tells you something else with the terms that they insist on, believe the terms.

The other way perceived risks manifest is if a term sheet includes non-standard or “dirty” economic terms. Here, the term sheet example is instructive not for what it contains but what it doesn’t. Examples of such terms would be:

- Liquidation preference greater than 1x — the investor gets back more than its invested capital first.

- Participating preferred — the investor double-dips by getting its money back plus its pro rata portion of exit proceeds, rather than choosing between the two.

- Cumulative dividends — the investor compounds its liquidation preference every year by X%, which increases the economic hurdle that has to be cleared before founders and employees see any value.

- Warrant coverage — the investor gets extra fully diluted ownership without paying for it at the agreed upon valuation.

These are all ways of adding structure to reduce typical venture risk, either directly by boosting the investor’s downside economics, or indirectly by juicing the upside outcomes. The investor is essentially saying, “I’m sort of afraid of losing my money.” It can also foreshadow how they might behave when things aren’t going well, such as pushing you to sell when you don’t want to, or dial back risk when it’s important to take it. Good investors would rather address economic risks by negotiating valuation, and are otherwise happy to give standard terms because they know that the real money in venture is not made with structure, but by building long-term value, which they are confident in their ability to help you do.

The last thing to remember is that your Series A documents are a foundation and precedent for the terms of future rounds. Good foundations make the next term sheet and financing round fast and simple, as future investors just step into the same straightforward terms. Doing the opposite complicates future fundraises, such as future investors asking for the same structure-heavy terms, existing investors refusing to drop terms that subsequent investors want removed as a precondition of investing, etc. Unwinding bad terms is difficult, and oftentimes impossible.

That said, the point is to get a clean deal, not to cycle a lot to get the perfect deal. No one ever built an enduring company just by winning their Series A negotiation. Also, even if you can’t get everything right or the way you want it, you always have the power to execute. If you do that, the value you build can outrun suboptimal terms or establish leverage to renegotiate later. So don’t lose sight of the ultimate goal: closing fast and getting back to work.

Notes

1. Some great investors still send longer term sheets, but this has more to do with their preference for going a bit deeper into the details at this stage, rather than deferring this until the definitive documents. The definitive documents are derived from the term sheet and are the much longer (100+ pages) binding contracts that everyone signs and closes on. It’s common to negotiate a few additional points at this stage, though deviation from anything explicitly addressed in the term sheet is definitely re-trading. Also, in a few places, this term sheet refers to certain terms as being “standard.” That may seem vague and circular, but term sheets frequently do describe certain terms that way. What that really means is that there’s an accepted practice of what appears in the docs for these terms among the lawyers who specialize in startups and venture deals, so make sure your lawyer (and the investor’s lawyer) fit that description.↩

2. The two most impactful investor vetoes in this section are the veto on a financing, which is covered by clauses (ii) and (iii), and the veto on a sale of the company, which is in clause (vii). We point these out because the concrete implications of these clauses aren’t facially obvious, and because most term sheets use similar technical jargon for these vetoes.↩

3. The founders implicitly control those 2 seats because they’re designated by a majority of common, and founders generally control a majority of common for a long time. In even more founder-friendly term sheets, those 2 seats may be designated by the founders themselves (as individuals).↩

4. Whether being fired from the company as an employee also triggers the removal of the founder from the board is a separate question and depends on what was negotiated in the financing documents. Sometimes a founder’s right to vote her shares to appoint a director will be conditioned on the founder being currently employed by the company. Whenever conditions are attached to your rights to vote on anything, make sure to ask your lawyer to walk you through the various scenarios in which those conditions matter and how they can hurt you.↩

This is not legal advice.

Thanks to Carolynn Levy, Jon Levy, and Nicole Cadman for their comments on this.